Monthly Undermining Task, March 2010: Throwing off the Shackles of Debt

Posted by keith on March 1st, 2010

by Guy R. McPherson, Keith Farnish, Dave Pollard, and Sharon Astyk

Indebtedness is a form of involuntary servitude and, in extreme cases, involuntary imprisonment. Consider, for example, the current usurious rates of interest (versus what savers earn on their savings in the same banks that charge that interest). Many religious organizations loath interest rates as immoral and criminal. According to all four gospels in the Christian bible, even the normally passive, peaceful prophet of Christianity got so worked up about usury in a temple he started acting like Alex Ferguson on the sidelines of a Manchester United football match.

Purchases by consumers (this awful word is used here only because that’s what we have become – involuntarily) drive the world’s industrial economy. And purchases by consumers depend on the confidence of those consumers, so that consumer confidence underlies commercial success. If a potential consumer has no confidence in her ability to purchase an item, then she won’t. If enough potential consumers lose confidence in their ability to purchase and pay for any particular item, the sales of that item will plummet, causing the manufacturer and sellers of that item to fail.

Considering the current financial situation, which will no doubt crash again within the next year, we can help create a situation that will both change behaviour for the better and prevent people from getting into financial trouble. The latter portion is vital to getting wide support for such activities, and will be a huge challenge for hopelessly optimistic, reality-challenged members of the industrial economy.

How do we convince people they definitely cannot afford to take out loans to buy things? More impact will be realized by targeting luxuries such as houses, cars, and appliances than small “goods.” Governments throughout the industrial world recognise this, and have therefore rewarded people for purchasing houses, cars, and — most recently – appliances, by giving them huge financial incentives (i.e. taxes on other taxpayers who might not even be tempted to play the “consumer” game).

Loans are required for most people to purchase these “durable goods” (which are no longer durable or good). Loans traditionally are seen as safety nets, but it has become clear they really represent traps. Never mind the psychological or ecological implications of consumerism — there exists no evidence suggests anybody has minded so far — the focus here is on the trap into which each potential consumer falls by taking out a loan to mindlessly invest in transient baubles. Every loan is a bad deal for the borrower, whether a straight money request, an HP deal, a mortgage or a credit card payment.

The system needs you to keep borrowing; if you don’t then who knows what could happen…

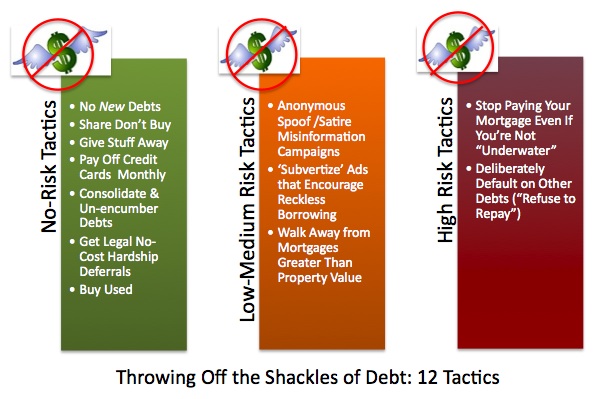

Note: The risk levels indicated below are approximate and will vary according to your personal situation and the jurisdiction you operate in. Always take legal advice if you are unsure.

No Risk:

Don’t take out a loan for anything. If you need it — and probably you don’t — save your money and buy it, barter for it, or borrow it.

Encourage others to join you. Start by sharing your car, your garden, your tools, even your clothes. Pass stuff on; give stuff away. You don’t need that loan and neither do the people you care about.

If you already have loans, and most recent students do, then seek deferral under economic hardship. Odds are pretty high you’re actually experiencing economic hardship, so this is no big deal. And even if you’re not, there’s no sense feeding the beast if the beast defaults down the road.

Low to Medium Risk:

Start a “misinformation” campaign (from the point of view of the loan companies):

1) Via snail mail, send out false press releases from loan companies and banks to media outlets such as local radio stations, local press and even the nationals if you are brave enough. These press releases should discourage people from taking out loans because, after all, people don’t really need all the toys they buy on credit. If you make the “press releases” as complete as possible, and word them so that responses are not required then there is a good chance they will be run without questions being asked.

2) Do a bit of subvertising, on the internet or (for a little higher risk) on billboards: focus on loans companies and banks changing the messages to emphasise the theft aspect of loans. Alternatively, just remove loan adverts entirely. For more information on techniques, read this post.

Other potential actions along these same lines include:

– Organising “default-ins” along the lines of the “love-ins” and “sit-ins” of the 1960s,

– Devising and publicising satirical fake get-rich-quick schemes that exploit government mortgage subsidies and the overvaluation of real estate: “Get £1 million in property free from Government mortgage subsidy scheme with no risk or money down!”; “Sell property short before the crash and make £1 million with no risk or cash!” and

– Helping to organise and formalise the exploding “grey” market for overpriced property: Thousands of people are moving or retiring and unable to sell their homes at anywhere near their mortgages, so they are renting out their homes for a fraction of current market rents, and likewise renting others’ homes in areas to which they are moving at far below market rents. Everyone hopes prices will somehow bounce back and save them from default. Eventually these homeowners will have to threaten default to get mortgage companies to write off the excess of mortgage value over real property values. We need to help them do that, and also help them find “grey” market properties in the meantime.

Obvious satirical routines can be developed for a variety of venues. This strategy should hold particular appeal to artists.

Medium Risk:

This is taken from Dave Pollard’s article ”Walking away from your mortgages”:

Many people are now living in homes with mortgages that are greater than the value of their property. Why would anyone continue to pay a debt that is higher than the asset it secures? After all, big corporations view pulling the plug on unsuccessful ventures and sticking the debtholders and shareholders a key business strategy. The whole idea of “risk capital” is that the interest and other fees you earn for lending to risky borrowers compensates you for the risk, so that if the borrower defaults you accept the loss and chalk it up to experience. Yet for some reason homeowners feel some moral obligation to throw good money endlessly after bad. This of course is exactly what the corporatists, who have no such moral compunction, are counting on, what economists call moral asymmetry. The logical response would be to tell the lender to write off the excess of the mortgage beyond the property value, and refinance the mortgage accordingly. Apparently in some US states (called “recourse” states) this moral asymmetry is institutionalized — that is, lenders can go after a mortgagee’s personal assets if they default. There is, of course, no recourse when the corporatists walk away from debts, offshore their operations, and stiff the taxpayers whose subsidies and bailouts paid for the corporatists’ ventures.

Where is the sense of outrage here? Have the education system and media so dumbed down the citizens that they can’t see this scheme for the cruel and criminal con it is? If everyone with a mortgage greater than the value of their home either walked away from it, or was legally empowered to require the excess to be written off as the “bad debt” it is, then of course there would be many bank failures and plunging profits. That’s how the market system is supposed to work. The lenders, of course, want it both ways, and Obama and the citizens seem blithely willing to let them have it.

Walking away from your mortgage entails medium risk because it will damage your credit rating. Obviously, this doesn’t matter in the long term, but it still causes concern for many people.

On the same lines as the lower risk snail mail press releases, via electronic communications, send out false press releases from loan companies to media outlets. These press releases would discourage people from taking out loans because, after all, people don’t really need all the toys they buy on credit. This requires a level of technical expertise as the instigator would need to hide behind an alter-ego and fake domain.

High risk:

Taking a step beyond abandoning your underwater mortgage, don’t pay off your mortgage even if you’re not underwater. Simply default but continue to occupy your house. Ditto for other loans. The lenders cannot afford to tell their stockholders about it, so the borrower gets the loan for no payments while the lender gets stuck. This idea was encouraged by the reporter who writes about housing issues for the New York Times when he stopped paying his mortgage (and wrote about it, nine months later, in the Times, by which time nobody had asked for a payment). At this point, the idea is receiving plenty of attention, and even CNBC is on board.

These actions are high risk because they could bring criminal proceedings related to fraud. Probably they won’t. But stranger things have happened, so we issue the following disclaimer:

The authors and the host of this web site do not condone any actions which break the law under the jurisdiction where the described activity is taking place.

Which, of course, doesn’t mean you shouldn’t do them at your own risk.

What we’re trying to do here is help bring down a house of cards: People feeling forced to pay debts far greater than the real value of the assets that secure them. People seduced into getting into debt needlessly. People paying usurious interest rates and fees because the banks own the politicans. It’s a debtors’ prison without locks and doors, and it’s immoral. Help us bring an end to it.

________________________

This essay is part of a larger collaboration between the authors. It represents the third month of the Monthly Undermining Tasks.

March 2nd, 2010 at 3:48 am

[…] KEITH FARNISH Monthly Undermining Task, March 2010: Throwing off the Shackles of Debt […]

July 11th, 2010 at 4:15 am

I’m surprised to see no mention of bankruptcy in this article – a perfect way of getting rid of debt and undermining the system. Of course, you can’t go this route if you have assets you want to hold onto or if you are likely to want to borrow in the next 6 years, but other than that there aren’t really any downsides. I think people still associate a certain stigma with it, but it really doesn’t exist anymore.

I did it 2 years ago and the sense of freedom it brought was immense. I highly recommend it to anybody.

July 14th, 2010 at 4:57 am

Hi Andy

I agree that bankruptcy can be a good option for many people, and we did discuss this option when writing the article (Guy, Sharon, Dave and myself) and decided that as it is being used a “get out of jail free” card by people then it could only be included with provisos that there are often complex repercussions that many bankrupts don’t realise – we are not financial advisors so were not really qualified to suggest this option.

However, as an undermining tool, it can probably work…

K.

January 20th, 2011 at 6:20 pm

Keith, ive only just come across this post. There is a lawful remedy to stop paying so called unsecured loans, credit cards etc. All agreements are not valid contracts because full disclosure hasnt taken place. Theres a growing number of people taking the bank fraudsters on. It needs to be known that they DO NOT “lend” you any money-you create it and they steal it via the Maritime Salvage legislation. It is worth watching the Money as Debt film on youtube and if i may point people in the direction of a very good site? http://www.getoutofdebtfree.org

All the best, Steve.

January 21st, 2011 at 5:35 am

Thanks, Steve. Very interesting information and thanks for the link.

K.