Co-operative Bank Breaks Own Ethical Policy With Millions Of Chinese Card Readers

Posted by keith on November 13th, 2009

I am under no allusions about the potential for “ethical” banking; unless you put your money into a bank that does not indulge in usary (such as banks that operate under Sharia Law) then someone, somewhere is being screwed, and most likely your bit of money is going to be having a negative impact on the natural environment. Non-Islamic banking is about making profit from someone else’s desire to keep their money safe, or make some interest themselves, but some banks are slightly less harmful than other banks.

Take the Co-operative Bank, based in Manchester, UK, which was founded on the principles of Cooperative Societies, and has maintained a set of evolving ethical standards since its inception in 1872. Lots of Environmental NGOs use the Co-op Bank for this reason, and up to very recently they seemed to put their money where their mouth was.

Here is their Ethical Policy, taken from www.goodwithmoney.co.uk, and broken down into the four core areas of Human Rights, International Development, Ecological Impact and Animal Welfare:

Human Rights

We will not finance:

* any government or business which fails to uphold basic human rights within its sphere of influence;

* any business whose links to an oppressive regime are a continuing cause for concern;

* any organisation that advocates discrimination and incitement to hatred;

* the manufacture or transfer of armaments to oppressive regimes;

* the manufacture or transfer of indiscriminate weapons, eg cluster bombs and depleted uranium munitions;

* the manufacture or transfer of torture equipment or other equipment that is used in the violation of human rights.

International Development:

We will seek to support poverty reduction. In line with this, we will not finance organisations that:

* fail to implement basic labour rights as set out in the Fundamental ILO Convention eg avoidance of child labour, or that actively oppose the rights of workers to freedom of association, eg in a trade union;

* take an irresponsible approach to the payment of tax in the least developed countries;

* impede access to basic human necessities, eg safe drinking water or vital medicines;

* engage in irresponsible marketing practices in developing countries, eg with regard to tobacco products and manufacture.

* Furthermore, we will support fair trade and the provision of finance to the working poor in developing countries via micro-finance.

Ecological Impact:

We will not finance any business whose core activity contributes to:

* global climate change, via the extraction or production of fossil fuels (oil, coal and gas), with an extension to the distribution of those fuels that have a higher global warming impact (eg tar sands and certain biofuels);

* the manufacture of chemicals that are persistent in the environment, bioaccumulative in nature or linked to long term health concerns;

* the unsustainable harvest of natural resources, including timber and fish;

* the development of genetically modified organisms where there is evidence of uncontrolled release into the environment, negative impacts on developing countries, or patenting (eg of indigenous knowledge);

* the development of nanotechnology in circumstances that risk damaging the environment or compromising human health.

Furthermore, we will seek to support:

* businesses involved in recycling and sustainable waste management;

* renewable energy and energy efficiency;

* sustainable natural products and services (including timber and organic produce);

* the pursuit of ecological sustainability.

Animal Welfare

We will not finance any organisation involved in:

* animal testing of cosmetic or household products or their ingredients;

* the exploitation of great apes, eg in experimentation or general commercial use;

* intensive farming methods, eg caged egg production;

* blood sports, which involve the use of animals or birds to catch, fight or kill each other;

* the fur trade.

Furthermore, we will seek to support:

* businesses involved in the development of alternatives to animal experimentation;

* farming methods that promote animal welfare (eg free range farming).

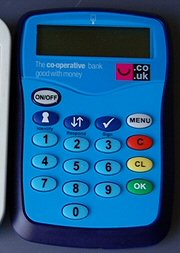

So imagine my surprise to find that throughout 2009 and into 2010, every single customer of the Co-operative Bank who uses Internet Banking would be issued with a secure card reader. “What’s wrong with that?” you may ask; and from a security point of view it’s actually a fairly sensible thing, if you know what you are doing — I used RSA SecureID tokens for years in my previous work.

The first problem is merely practical: most people really don’t need another level of complexity in their life. Pay a bill online, and previously you would go through a two layer security model, complete with secure two-way authentication and encrypted communications. All of this was automatic apart from entering your account details and the answer to a personal question: now you have to carry out further two-way authentication, manually, and enter the pass code on screen. Guaranteed to ensure people start writing their account details and personal answers down above their computer so they have less scrabbling around to do.

But The Unsuitablog has another, far more sinister problem with the card readers.

Approximately two million of these pocket-sized devices are being given out by the Co-op, and many more will subsequently have to be replaced. The devices are known as Xi-Sign 4000, and are produced by a French company called Xiring. This company produce the vast majority of card readers issued to customers of UK banks; so you can be pretty sure there are tens of millions of these little electronic gadgets floating around in the UK alone. The mind boggles to think how many they might have produced globally!

From the Co-op Bank’s point of view, there are a couple of little problems:

“We will not finance any business whose core activity contributes to global climate change…”

Ok, there may be the proviso that they don’t invest in extractive industries alone, but to me that’s a complete cop-out. Each Xi-Sign 4000 is made from oil, and the production of it requires electricity which is generated predominantly through the burning of climate changing fossil fuels. Had the card readers not been issued, then an awful lot of climate changing gases would not have been released, or oil squandered.

Turn the card reader over and you will see “Made in PRC”. Yes, that’s two million devices made in China, which immediately wipes out another of the Co-op’s key policies:

“We will not finance any business whose links to an oppressive regime are a continuing cause for concern”

Quite cleverly worded, here, because they don’t explicitly say that just any link to an oppressive regime may be a cause for concern, but instead imply that only certain types of link may be a cause for concern. That’s just crappy semantics, as far as I’m concerned: if a regime is oppressive — and the government of China is one of the most oppressive regimes on Earth — then any link, including working within its political boundaries is a cause for concern. Simply by supplying products made in China, the Co-op have violated their own policy.

And there is more. China’s electricity is about 80% coal generated, therefore the first policy violation is even more blatant: the Co-op, by supplying Chinese card readers, are supporting the extraction and burning of climate changing coal. In addition, with the other 20% coming from a series of huge dams, that have been constructed with massive loss of human habitation and violation of the basic right of a place to live, the Co-op have violated yet another policy:

“We will not finance any government or business which fails to uphold basic human rights within its sphere of influence”

How would you feel if your money had been invested in a project that displaced millions of people from their homes?

As I said, there are many other banks who don’t have any ethical policies, and certainly don’t stick to those they have in any meaningful way; but if you are the Co-operative Bank, who for decades have traded on the mantle of “Ethical Banking” then you had damn well better stick to your principles, or be tarred with the brush of Ethical Hypocrites.